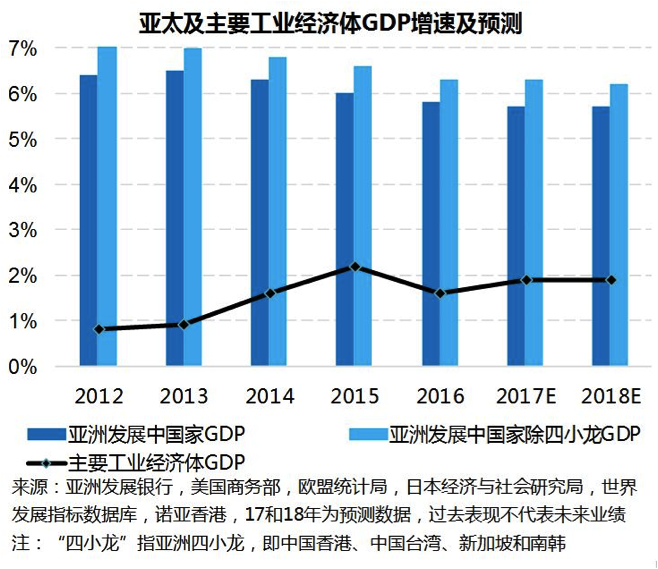

Over the years, the overall GDP growth of developing countries in the Asia Pacific region accounts for over 60% of global GDP growth. In the 16 years, the growth rate of GDP in the GDP of developing countries in the Asia Pacific region was 5.8%. In the case of China's GDP growth rate decreasing, 30 of 45 Asia Pacific economies still maintain good growth trend, mainly due to the increase of external demand stimulated trade growth and the increase of global commodity prices. We expect the Asia Pacific to continue to maintain an overall GDP growth rate of 5.7% in the 17 and 18 years. After removing four Pacific dragons (South Korea, Singapore, Hongkong and Taiwan), GDP growth in the Asia Pacific region is expected to reach 6.3% and 6.2% in 17 and 18 years. The growth rate of GDP in China for 17 and 18 years is expected to be 6.5% and 6.2% respectively.

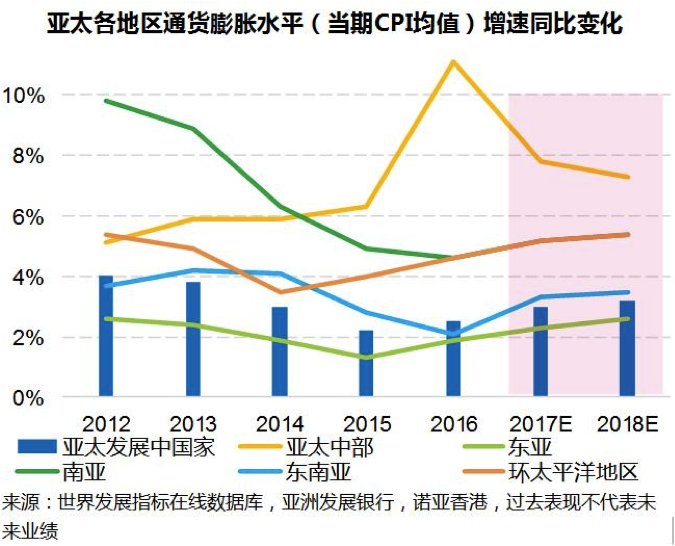

In the context of strong consumer demand and the recovery of global commodity prices, the rate of inflation in the developing countries of the Asia Pacific region in 16 years is 2.5%. It is estimated that inflation will continue to increase, and it will reach 3% and 3.2% in 17 and 18 years, respectively. Part of the Asian central Asian countries' large devaluation will also be one of the reasons for the overall inflation level in the Asia Pacific region. The overall level of inflation is more reasonable, the rising rate is mild, lower than the ten year average of 3.9% in the Asia Pacific region, and it is not expected to affect the relatively stable price level in the Asia Pacific region. China's exports have begun to decrease, and economic growth is more dependent on domestic demand. China's economic structural transformation has continued. The focus of economic growth has shifted from industry to service industry, and the economic growth rate has been slowing down. The government will put the maintenance of economic and financial stability first and accept the slow decline in the GDP growth rate. China's recent anti corruption actions against financial regulators are especially obvious before the "Nineteen big". In the long run, it will help China's economic development and transformation of its economic structure. China's money supply showed a downward trend compared with the same period last year, which is consistent with China's policy of deleveraging and the suppression of financial and real estate bubbles, which is also one of the reasons for the decline of China's economic growth. We expect China's GDP growth rate in 17 and 18 years to be 6.5% and 6.2%, respectively.

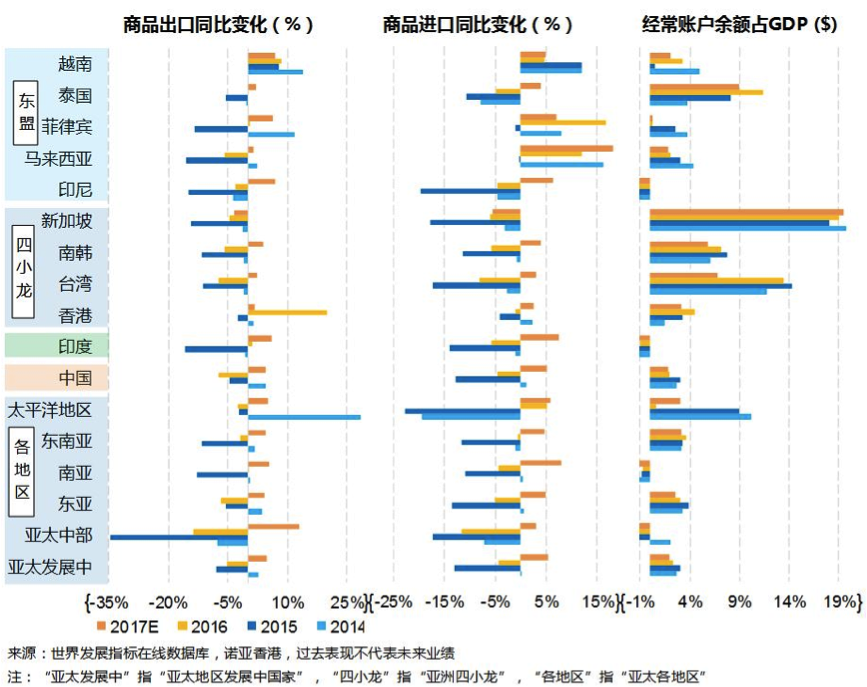

In November 16, the government of India decided to abolish the large bills and suppress some trading activities which India strongly relies on cash transactions, but the impact will only be temporary. India's economy will resume high growth after its short liquidity squeeze. The government's deregulation after the waste note movement and its tax reform on goods and services will also enhance the confidence of consumers and investors, and then increase business activities and investment activities and promote economic growth. India's economy will return to high growth after a transient liquidity squeeze. We expect India's GDP growth rate in 17 and 18 years to be 7.4% and 7.6%, respectively. In the four Asian dragons, the money supply in Singapore and Hongkong showed an upward trend compared with the same period last year, which helped to increase market liquidity and reduce interest rates, which is conducive to economic development, while Taiwan and South Korea showed a downward trend. The monetary supply of the association of Southeast Asian Nations has been rising slowly over the same period, which is conducive to the smooth development of the economy. Despite the resumption of exports in the Asia Pacific region, its current account surplus is expected to continue to decrease. The Asia Pacific current account surplus in 16 years is 0.7%, and it is expected to be less than 0.5% in 17 and 18 years. Although exports from many Asian Pacific countries have begun to recover, especially in the traditional manufacturing export countries, the import volume has increased faster. China's economic structural adjustment led to export weakness, which is also one of the important reasons for the reduction of exports in the Asia Pacific region.

Although the US's attitude towards trade in China and the Asia Pacific region has been slightly milder recently, the risk of trade conflicts and the increase of tariffs in the US still remain, which is a blow to the trade, investment and export in the Asia Pacific region. The economic recovery of the euro zone is more obvious, and the results of the Holland and French elections are helpful to the growth of investment in the eurozone and the stability of consumer confidence. The British Prime Minister, proposed in June 8th early elections, in order to increase the stakes in Europe and to discuss the domestic support and the British, the British political uncertainty remains high at present. Japan's exports are growing, and if they are maintained, it will support a sustained recovery in its economy. With the increase of consumption and economic activities in the United States and the fiscal stimulus and tax reduction policies Trump will implement, the US economy will grow better in the 17 and 18 years. We expect the fed to increase its interest rates in June and September, and to expand the table for a period of 2-3 years at the end of the year. The Asia Pacific countries need to be vigilant about the negative impact of the Fed's tightening policies on economic development. On the one hand, the Fed's tightening policy will bring some capital outflow risks to some Asian and Pacific countries. On the other hand, once the debt is mature, many borrowers need to borrow the new debt or renew the debt, while the higher interest rate will increase the cost of reimbursement and affect its repayment ability. Higher interest expense will also reduce consumers' purchasing power and investors' desire for financing, and consumer confidence and investment enthusiasm will be compromised. Domestic demand will also decline, which will have a negative impact on economic growth. Next, we further analyse the pressure that the Asia Pacific countries face in these two aspects.

First, the impact of American interest rate increases and shrinking tables varies from different countries to different rates of exchange rate mechanisms and corresponding dynamics. Once the expected rate of increase in interest rate and the process of shrinking the table are expected, the value of non US dollar denominated assets will shrink, which will lead to capital outflow, combat consumer and investor confidence and affect the economic stability of the Asia Pacific economies. The Asia Pacific countries may require substantial increases in interest rates, in order to reduce the outflow of capital to the United States, causing the interest rate and liquidity of global tension, higher financing costs, and promote active currency appreciation, it may cause adverse effects on exports, both will influence the economic development. We expect the Fed will not be too radical to raise interest rates, although recent inflation in the United States has risen, but it is not enough to be a reason to accelerate interest rate hikes. Only if there is a higher growth in the real economy and the GDP, the Fed may consider increasing the intensity and number of interest rate increases. Even if Trump implements the promise of his campaign and implements fiscal stimulus and tax reduction policies in the second half or 18 years of 17 years, the new policy will take a period of time to see the effect and stimulate the substantial growth of the real economy. At the same time, it is worth noting that although the US liquidity tightening policy will further push up the US dollar exchange rate, the Asian Pacific countries' currencies will depreciate against the US dollar, but the devaluation extent of different countries will be greatly related to the exchange rate mechanism of the country. Countries that implement foreign exchange control will abandon the relative export advantage brought by the large depreciation of currencies in exchange for macroeconomic stability, while currency devaluation will also exacerbate inflation. In the case of smaller or slower interest rates and smaller scale, we expect Asian Pacific countries to slow down capital outflows without slowing economic growth.

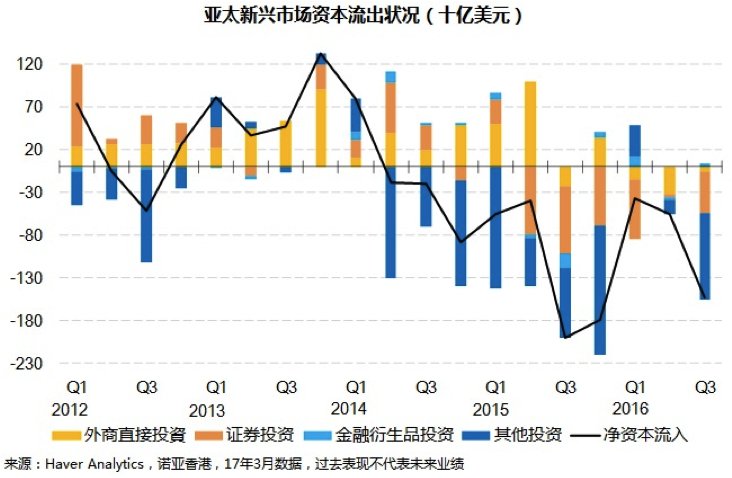

It is worth noting that the emerging markets of the Asia Pacific have begun to experience net capital outflows since 14 years. The capital flow of China is leading the capital flow of the whole Asia Pacific region. At the beginning of the 14 and second quarter, China has generated 35 billion dollar net capital outflow from its banking and investment activities. In the third quarter of 16 years, the net outflow of capital has exceeded 130 billion US dollars. With the increase of Chinese investors' overseas investment and the decrease of overseas investors' investment in China, China's outward foreign direct investment has also become a net outflow in the second half of 15 years. It is particularly noteworthy that although the Asia Pacific region shows a trend of net capital outflow as a whole, there is a positive net inflow of FDI in overseas direct investment projects led by India, Indonesia and Vietnam, which are favored by overseas investors. Although this year, due to increase in the capital market of developed country is larger, higher valuations, Asia Pacific countries capital market with excellent performance and valuation is more reasonable, so as to attract capital inflows, we expect the Asia Pacific developing countries will continue throughout the year a net outflow of capital. With the global economy growing, uncertainty has become the main investment theme for investors for 17 years. The US economic recovery and its policy of increasing interest rates and reducing the balance sheet will attract Asia Pacific Capital to the United States. The trend of the devaluation of the RMB is also one of the driving forces of the past two years. Although the United States to reduce domestic liquidity to other countries in the Asia Pacific caused by capital outflows, the implementation of other developed countries, monetary policy can slow the pressure, reduce the Asia Pacific countries to raise interest rates to control capital outflows and leave more space for the economic growth of the Asia Pacific countries.

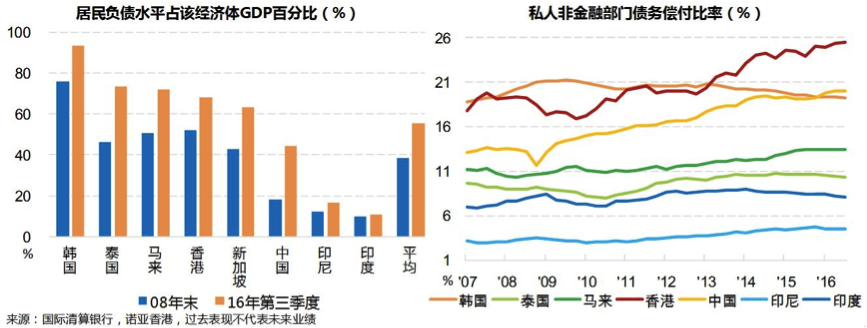

Second, countries with high debt ratios in the Asia Pacific countries will become more vulnerable when liquidity cuts and capital costs rise. Most Asian economies have greater growth in the 08 years after the debt level, consumers are more inclined to western consumer debt mode, household debt levels accounted for the proportion of GDP increased nearly 91%, of which South Korea from 08 years to 74% years rose to 16 in the third quarter, Malaysia and Thailand in the third quarter of 16 years up to approximately 71% high. In the third quarter of 16 years, the proportion of residents' debt to GDP has been more than two times more than the 08 year level, and it has reached 50%. Although Hongkong, Malaysia and Indonesia, China private non-financial sector debt ratio is rising, South Korea's private non financial sector debt ratio in 09 years has declined, while Thailand and India in 14 years also decreased, even lower than 6 in indonesia.

At present, because these countries economic growth and employment levels are generally good, asset prices relatively stable, banking financing environment is relatively good, the rate of bad loans is relatively low, so the risk accumulation of high debt is not reflected, but once the liquidity crunch, the economic environment becomes worse, it may appear a series of chain reaction. Therefore, these countries should implement or strengthen macro prudential policies, such as reducing the ratio of the income of the residents and the ratio of the enterprise loan assets. Policymakers should also conduct regular stress tests on the banking sector to track the total amount of bank loans and to confirm whether they need a bank to extract special reserves. These countries even need to intervene in the real estate market to curb speculative demand and reduce asset bubbles. We believe that the Asia Pacific countries will further consolidate and expand their economic development advantages.

(the author: Xia Chun and Zheng Jiachuang are the chief research officer and analyst of Noah International (Hongkong) research company. This article only represents the author's point of view.)